Jane Aavik, Head of Business Customer Segmentation at LHV, gives an overview of payment trends in 2026 and what technological and legal changes will affect the daily payment experience of both e-merchants and consumers in the coming years.

The world of payments is changing fast. The coming years will shape how we pay in the future, how merchants accept money, and how countries impose requirements on payment infrastructure. Digital wallets are gaining more and more popularity in Estonia, both in physical and online stores. With low prices and a wide product range, Chinese online stores have made themselves an attractive alternative in the West. Fraud prevention has also become an important topic in society.

Trends in Europe

2026 will be the year of infrastructure, especially in the area of digital payments. There are three major directions that are moving forward simultaneously: these are instant payments, digital identity, and the regulatory environment of the payment market.

Instant payments are becoming the new norm in Europe. The Council of the European Union’s new Instant Payments Regulation now requires banks and payment service providers to support real-time euro payments around the clock, including outside business hours.

In addition, the verification of the bank account number, i.e., the name of the owner of the IBAN, has entered into force. This will help prevent fraud and payments to the wrong payee (European Central Bank, 2025).

At the same time, the new framework for payment services (PSD3/PSR) is progressing in the European Union. This is necessary to strengthen consumer protection and introduce new refund rules against identity fraud (VinciWorks, 2025).

The third big change concerns digital identity. Through the European Digital Identity and Trust Framework (eIDAS2) and the European Digital Identity Wallet, the solution will be designed as a ‘log in and pay’ standard, making user authentication and payment one seamless step (Europa.eu, 2024). The future digital wallet will allow people and businesses to securely store their identity and credentials and use them for both public and private services, including payment services.

All of this raises the question of the role of artificial intelligence in security. AI-based fraud and risk models assess payments in real time to detect unusual behaviour, device risk, and suspicious patterns.

Specificity of the Estonian market

Last year, Estonia’s e-commerce revenue grew by 18 percent, reaching € 5.4 billion (ERR, 2025). In the same article, the head of the Estonian E-Commerce Association stated that e-commerce grows by 10–20 percent annually, and is expected to account for 40–50 percent of total trade within the next decade.

In Estonia, innovation in the area of payments is generally developing at a fast pace. The banks and payment service providers here are at the forefront of the introduction of fast payment methods in Europe, and our consumers expect easy and convenient solutions. Bank payments (open banking payments) are increasingly competing with payment cards. This means lower fees for the merchant and faster settlement for the client.

Digital wallets also increasingly popular in e-shops

Today, 53% of online purchases worldwide are made with digital wallets such as Apple Pay, Google Pay and Alipay. According to forecasts, their share will increase to 65% by 2030. However, credit card payments decreased by 9% in 2024 compared to 2023 in terms of global online sales (Capital One Shopping, 2025).

According to the Capital One Shopping provider, the payment method ‘buy now, pay later’ is most popular in Sweden, where around 23% of online transactions are made in this way.

In LHV’s business customer segment, we consider it likely that digital wallets will sooner or later become the leading e-commerce payment method in Estonia. At present, the average Estonian person is still stuck in old habits and prefers bank payment in the e-shop. However, Apple Pay and Google Pay are faster and more painless payment methods due to the use of biometric identification. We are convinced that speed in payment is exactly what our buyers will appreciate in the future.

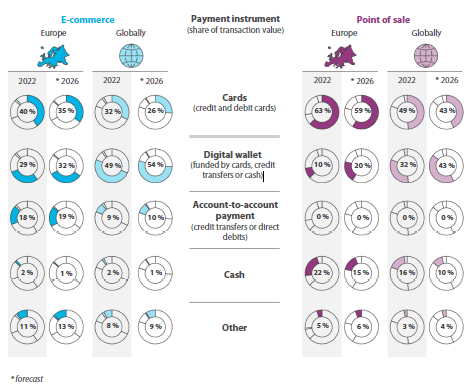

We can see from the European Court of Auditors’ digital payments overview graph that while the value of payments through digital wallets is growing strongly, the growth in bank payments is becoming smaller and smaller. The number of payments made with cards in e-shops is also decreasing in Europe.

Figure. Breakdown of transaction value by payment instruments. Source: ECA, based on the 2023 FIS Global Payments report.

The competition between cards and digital wallets could rise to critical levels by 2030, with these two payment methods struggling for a global market share in Europe, according to data from the U.S. fintech company Worldpay and Payments and Commerce Market Intelligence (PCMI), a payment and commerce market analysis company (PCMI, 2025).

Chinese e-shops gaining market share in Estonia

Estonian e-commerce has been strongly influenced in recent years by the rise of Chinese platforms. According to Omniva, the volume of parcels ordered from China increased by around 40% in 2024, and is mainly driven by Temu, AliExpress and Shein (ERR, 2024). Low prices and a wide product range have made these e-shops an attractive alternative, especially during the cooling of the economy.

At the same time, the European Union is moving towards abolishing the tax exemption for low-value shipments (European Parliament, 2025). This could already reduce the price differential between European and Asian shops next year, and lead to fairer competition.

For European and Estonian merchants, this is an opportunity to stand out: faster delivery, a clear final price and reliable service are local advantages that foreign platforms cannot always offer.

Fraud prevention in e-shops

If consumers prefer to shop more and more online, this will lead to a negative effect of increasing fraud. It has, therefore, been necessary to introduce new legal requirements to deter criminals.

Making it compulsory to check the correspondence between the name of the payee and the account number already mentioned will reduce the amount of payments made to the wrong payee (European Central Bank, 2025).

With the entry into force of the new European Union payment framework, the consumer will have the right to a refund in cases where a third party has unlawfully acted as an employee of a bank, or a private or public institution, and, as a result of this mistake, the consumer makes an otherwise authorised but fraudulent payment (Finologee, 2025).

According to Lauri Teder, CEO at LHV Paytech, fraud rates in Estonia are on an increasing trend and are becoming more complex. However, old, familiar scams have also not disappeared. “Each of us needs to monitor our banking transactions closely and react quickly if any of them seem suspicious,” said Teder.

Starting from November, LHV Pank has a new security function for e-shop payments. Namely, the client receives a warning from the bank before confirming the payment if the payee is on the black list of the Consumer Protection and Technical Regulatory Authority.

In addition, Lauri Teder advises merchants to make smart use of the fraud protection module on the payment collection platform. This tool allows the seller to set up appropriate fraud prevention rules for their e-shop.

What next?

The digital payments landscape will change faster than ever before in 2026. New legal requirements, digital wallets and instant payments are driving developments in Europe. In Estonia, these are accompanied by a strong technical readiness and the expectation of local consumers to receive an immediate and fast service. Consumers increasingly prefer digital wallets both globally and, presumably, in the Estonian market.

The European Union is planning to abolish the tax exemption for low-value shipments, which could reduce the price difference between local and Asian e-shops as of next year, thus leading to fairer competition. On the other hand, businesses need to be vigilant as fraudsters become increasingly clever. The winners are those e-merchants who are able to provide a smooth, secure and transparent payment experience.